A dividend is a payment from a limited company to the shareholders.

There are some rules about when and how much the company can pay.

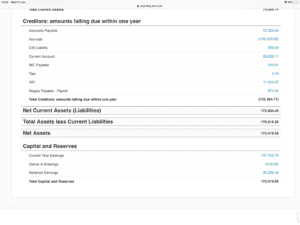

Rule 1 – There must be sufficient reserves available to distribute. Put simply, the company has more assets than liabilities. If you have accounting software, this is what to look for:

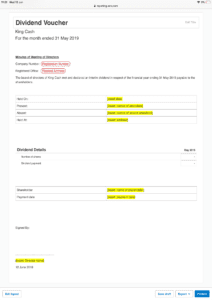

Rule 2 – Any declaration of dividend should be recorded on a voucher detailing how much per share, for which share type, who was present and the date of declaration. Here’s an example (again its from an accounting system, such as Xero that does all this for you).

Dividends that are declared do not necessarily need to be paid in physical cash but instead can be moved to a directors’ loan account to draw down on when they need it. This is often a good form of tax planning. You still pay tax as if you received it on the date declared. For example – you declare a dividend on 31 March 2018 but take the funds out on 12 August 2018. You pay tax on your tax return for the 5 April 2018.

If however, you take money from the business as a dividend and later realise there wasn’t enough reserves to do this (this is called an illegal dividend) then you will have to treat it as if you have just borrowed money from the business until the company can pay you a dividend or you can put the physical cash back in.

This does come with its own set of problems;

- You will need to pay a withholding tax called S455. This is a tax paid by the company on the balance you owe it at 32.5% if it is not repaid within 9 months. The company will get this back once the balance has been cleared.

- You will need to either complete a P11D return and pay tax and NI (both employee and employers) or

- Charge interest on the balance owed at a minimum of the official rate of interest.

Getting out of this situation can be quite difficult and a plan should be put in place to improve the business performance, coupled with reducing the money taken by the director. You have got to be very strict with the plan to avoid delays, which lead to further cash flow issues arising from the S455 tax and interest.

If you are a business in this position and don’t know what to do, contact us here.

This article is for general information only and does not constitute advice. Please do not take or refrain from action based on its contents. Information is based on our understanding of legislation at the date of publish and may change in future.